How Big Ten Programs Are Spending Millions on NIL Lawyers, Agents, and Consultants

A detailed look at how Big Ten athletic departments use consultants for compliance, confidential searches, and ticket sales algorithms to increase revenue, with real case studies and named consultants and roles.

Big Ten athletic programs operated like family-owned businesses for many years, but the incredible growth rate and attendant risks created opportunities for consultants to assist with legal, technical, fundraising, and ticket-price optimization. As the Big Ten grows in size and budgets, successful departments are remaking themselves to resemble professional sports franchises, and rightly so.

The Budget Behind the Budget

Public-facing athletic department finances tell a clean story. Revenue, expenses, coaching salaries, and facility costs. It all looks structured and contained. That version of the budget is real but incomplete.

There is another layer that sits underneath it, harder to isolate and rarely discussed directly. It shows up in procurement logs, board approvals, and capital project summaries, usually buried under categories like professional services or planning. This is where consultants live. Not as occasional hires, but as a recurring cost of operating at the top of college athletics.

The Big Ten, with its combination of massive media revenue and large public institutions, offers one of the clearest windows into that system. Enough information exists through public records and standard contract structures to piece together how outside advisors shape decisions across hiring, NIL, facilities, and long-term strategy.

What emerges is not a loose collection of engagements. It is a pattern.

Where Consultants Enter the System

The easiest place to see consultants is in hiring, because the process is visible by design. When a university announces a national search, it is signaling that the decision has been routed through an external framework. That framework typically includes candidate vetting, compensation benchmarking, and a layer of insulation for university leadership.

At the University of Wisconsin, the hiring of Chris McIntosh followed that script. The outcome leaned internal, but the process ran through a structure that gave it broader legitimacy. That is the point of the exercise. The search is not just about finding a candidate. It is about validating the decision in advance.

That same logic extends outward. Once salaries push into eight-figure territory, the idea of “market value” needs to be documented. Consultants provide it.

The NIL Shift and the Rise of Advisory Networks

Hiring is the visible edge of consultant use. NIL is where it becomes unavoidable.

When athletes gained the ability to monetize their name, image, and likeness, the existing structure of college athletics did not adapt gradually. It broke open. Departments that had never managed compensation systems suddenly had to think in terms of payroll, tax exposure, and donor-driven funding streams.

That gap did not get filled internally. It got outsourced.

Firms like Huron Consulting Group expanded their role in collegiate athletics by offering financial modeling and strategic advisory tied directly to NIL and revenue sharing. At the same time, large law firms such as Kirkland & Ellis and O'Melveny & Myers became part of the ecosystem, structuring agreements and navigating compliance boundaries that remain unsettled.

What makes NIL different from earlier consulting categories is where it sits. Much of the work does not run through the athletic department itself. It flows through collectives and affiliated organizations, which retain their own advisors. That structure makes the consulting footprint harder to measure but also more pervasive.

The system functions because multiple layers of advisors are working at once, often without appearing on the same balance sheet.

Following the Paper Trail: What FOIA Actually Reveals

Public records provide a partial but useful view into how this operates in practice.

At the University of Michigan, consulting activity tends to surface inside capital projects rather than as standalone contracts. Stadium and facility upgrades include feasibility studies, donor analytics, and premium seating strategy, all of which rely on external firms. The costs are not always itemized cleanly, but standard fee structures suggest that advisory services account for several percentage points of total project value. On projects exceeding $200 million, that translates into millions of dollars in consulting fees.

The Ohio State University provides a more distributed record. Vendor disclosures show recurring engagement with professional services firms tied to financial advisory, operational modeling, and legal work. Revenue strategy, particularly in ticket pricing and sponsorship valuation, often aligns with firms like Navigate, which specializes in modeling how pricing decisions translate into actual revenue.

At Penn State, the evidence appears less in vendor lists and more in board-level materials. The ongoing discussion around Beaver Stadium redevelopment includes references to feasibility analysis and phased planning, indicating outside involvement. At that scale, the absence of consultants would be more notable than their presence.

None of these records provides a single, definitive number. What they show instead is repetition. Consulting services appear across projects, across departments, and across decision types.

What It Costs to Operate This Way

Even without perfect transparency, the cost structure can be estimated with reasonable confidence.

At the top of the conference, programs like University of Michigan Athletics, Ohio State Athletics, and Penn State Athletics are likely to spend well into the eight figures annually when consulting is aggregated across legal work, capital projects, and strategic advisory services. The baseline sits lower in years without major construction, but the spikes during facility cycles are substantial.

A single stadium project can generate consulting fees in the range of 5 to 10 percent of the total cost when all advisory layers are included. That figure alone can reach into the tens of millions over the life of a project.

Mid-tier programs such as University of Wisconsin Athletics and University of Maryland Athletics operate with smaller yet still meaningful budgets, often spending several million annually, depending on the activity.

Programs that take a more controlled approach, including the University of Iowa Athletics and Northwestern Athletics, maintain lower baseline costs but still incur large consulting expenses when major projects or external reviews arise.

The consistent element is not the exact number. It is a fact that the number exists every year.

Big Ten and the SEC: Same Tools, Different Systems

Comparing the Big Ten to the Southeastern Conference reveals less about spending levels and more about structure.

Big Ten programs tend to formalize consulting relationships. Engagements are documented, processes are defined, and decisions are routed through frameworks that emphasize validation. That approach aligns with the governance style of large public universities.

SEC programs rely on many of the same firms and advisors, but the structure is less visible. Booster networks, internal leadership, and long-standing relationships carry more weight, and consulting often integrates into those channels rather than appearing as a formal layer.

In NIL, the contrast becomes sharper. SEC collectives often operate with greater autonomy, which can obscure the advisory network behind them. Big Ten programs, by comparison, tend to maintain more formal alignment between institutional strategy and external consulting.

Both systems use consultants heavily. They just incorporate them differently.

Does Any of This Translate to Winning

The temptation is to draw a straight line between consulting spend and on-field success. The reality is more complicated.

Programs with the highest levels of consulting engagement also tend to dominate in revenue, recruiting, and competitive outcomes. That correlation is real, but it does not mean consultants are the cause. They are part of a broader system that includes resources, brand strength, and institutional commitment.

What consultants do provide is leverage. They refine pricing, structure financial flows, and reduce uncertainty in high-stakes decisions. That creates incremental advantages that accumulate over time.

Programs that use consultants well tend to make fewer unforced errors. They allocate capital more efficiently and adapt more quickly to structural changes like NIL. That does not guarantee championships, but it raises the floor.

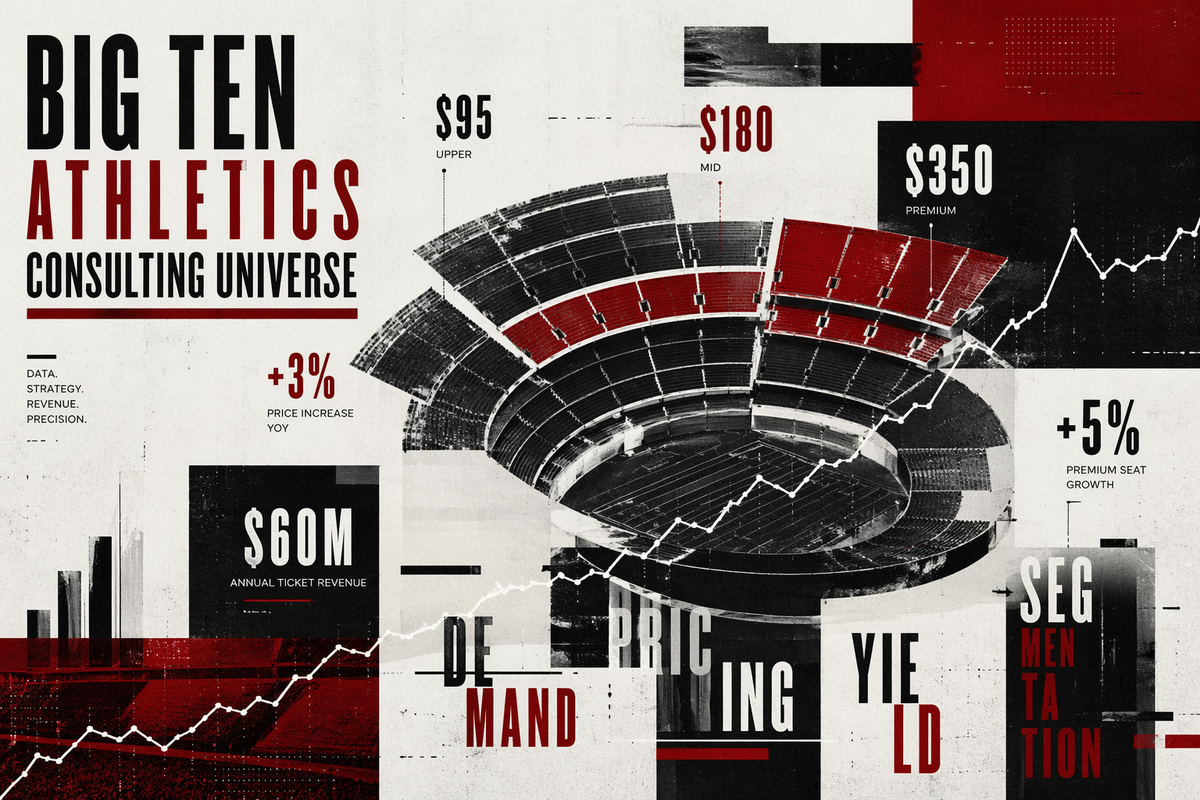

Ticket Revenue Consultants in Big Ten Athletics

For a long time, ticket pricing in college sports was set once and left alone. Athletic departments would tweak numbers year to year, maybe bump rivalry games a bit higher, and call it good. That approach no longer holds up in the Big Ten, where stadium size, secondary markets, and donor-driven seating have made tickets a far more complex revenue stream.

What changed is not just demand. It is how that demand gets measured. Instead of relying on instinct or historical pricing, departments now rely on outside firms to model fan behavior. The difference shows in the margins, and in this conference, the margins are large enough to matter.

What Ticket Consultants Actually Do

The work starts with data, and not just internal sales data. Firms like Navigate and Legends pull in resale platforms, historical attendance, opponent strength, kickoff times, and even weather patterns. The goal is to understand not what a ticket “should” cost, but what people have already proven they will pay.

From there, the model builds a demand curve. That curve shows where price increases hold and where they start to break demand. The useful part is rarely dramatic. It is finding a quiet space where prices can move a few percentage points without triggering a drop in attendance or renewal rates.

The second layer is segmentation. Not all seats behave the same way. Lower bowl inventory, club seating, suites, student sections, and single-game buyers all respond differently. Consultants break those groups apart and price them independently. What used to be one market becomes five or six overlapping ones.

Most departments do not run this as a fully dynamic system year-round. More often, a consulting firm helps build the framework, tests it across a season or two, and then the department manages it internally, bringing the firm back when something shifts.

Case Study: Ohio State Athletics Scale Turns Small Changes into Real Money

Ohio State does not need help selling tickets. What it needs is precision. With Ohio Stadium pushing past 100,000 seats, even a modest adjustment carries weight.

Over the past several seasons, average ticket pricing has trended upward in small increments, often in the range of three to five percent, depending on opponent and seat location. That does not sound like much until it is applied across a full stadium and a full home schedule. On a baseline of roughly $60–$70 million in annual ticket revenue, which aligns with public financial reporting ranges, those incremental increases can generate an additional $2–$4 million in a single season without materially affecting attendance.

Where consultants come in is identifying where those increases can stick. Resale data has been especially useful. When tickets for certain games consistently clear above face value on secondary markets, it signals that the department has been underpricing. Adjustments follow, usually spread across sections rather than applied bluntly.

The result is not a dramatic jump in pricing. It is a steady climb that captures value that would otherwise move outside the department’s control.

Case Study: University of Michigan Athletics Premium Seating as the Real Growth Engine

Michigan’s overall ticket demand remains strong, but the more interesting story sits inside the premium tiers. Club seating, suites, and donor-linked sections have driven a disproportionate share of revenue growth over the past decade.

Public financial disclosures place Michigan’s ticket revenue in a similar band to Ohio State, generally north of $60 million annually, but that figure understates where the gains are happening. Premium inventory carries significantly higher margins, and pricing there is less sensitive to short-term performance swings.

Consultants working with programs like Michigan focus less on general admission and more on structuring these premium offerings. Instead of asking what a seat should cost for one season, they model the value of a donor relationship over five or ten years. That changes the pricing conversation entirely.

In practical terms, a reconfiguration of premium seating or an adjustment in donation requirements tied to access can generate several million dollars in incremental annual revenue, even if total attendance stays flat. That is where much of the growth has come from, and it is not driven by gut instinct.

Case Study: Penn State Athletics Managing Volume and Variability

Penn State operates on a similar scale to Michigan and Ohio State, but with slightly greater variability in team performance and scheduling. Beaver Stadium regularly draws large crowds, yet pricing has historically been more conservative.

Recent adjustments have followed a familiar pattern. Incremental increases tied to opponent quality, combined with more aggressive pricing in lower bowl sections, have pushed total ticket revenue into the $50–$70 million range in strong seasons. The movement has not been linear, but the trend is upward.

Consultants play a role in smoothing that variability. By modeling demand across different scenarios, they help the department avoid overpricing weaker games while still capturing value in high-demand matchups. The goal is less about maximizing any single game and more about stabilizing revenue across the season.

That approach tends to produce smaller year-over-year jumps, but more predictable results.

Case Study: Northwestern Athletics Pricing in a Constrained Market

Northwestern faces a different problem. Demand is not guaranteed, and the market behaves differently than in larger football-driven programs. That shifts the role of consultants from optimization to calibration.

Ticket revenue at Northwestern has historically trailed the conference leader by a wide margin, often falling below $20 million annually, depending on performance and venue conditions. The Ryan Field redevelopment project introduces a new variable. Reduced capacity paired with upgraded facilities creates the potential for higher per-seat revenue, but only if demand follows.

Consultants in this context focus on scenario planning. What happens if attendance improves modestly versus significantly? How should pricing respond in each case? The risk is overestimating demand and pricing out the existing base without replacing it.

Early projections tied to the redevelopment suggest that even a moderate increase in average ticket price, combined with improved premium offerings, could add several million dollars annually. Whether that materializes depends less on the model and more on sustained engagement from the fan base.

Where the Gains Actually Come From

Across these programs, the pattern is consistent. Revenue growth does not come from dramatic changes. It comes from precision applied at scale.

A three percent increase across a large stadium can produce millions. A shift in how premium seating is structured can do the same. Capturing value that previously leaked into resale markets adds another layer.

Consultants operate in those spaces. They do not create demand, but they measure it more accurately than internal systems alone tend to allow. That measurement leads to adjustments that are small enough to go unnoticed by most fans but large enough to matter in aggregate.

The Broader Implication

Ticket pricing has moved from a static decision to a managed system. Once that shift happens, it rarely reverses.

Big Ten programs are not just selling seats anymore. They are managing inventory, segmenting customers, and optimizing revenue streams in ways that increasingly resemble those of professional sports. Consultants provide the framework for that transition, whether they remain involved long term or simply set the structure in place.

The effect is cumulative. Each small adjustment builds on the last, and over time, the difference shows up in budgets that continue to expand even when attendance remains steady.

The System Beneath the System

The most important takeaway from the available data is not tied to any single contract or firm. It is the pattern's consistency.

Consultants appear in hiring when decisions need validation. They appear in NIL when systems need to be built. They appear in facilities when investments stretch across decades. They appear in legal work when risk increases.

Over time, that repetition creates something that looks less like outside assistance and more like a parallel layer of governance. Decisions are still made within athletic departments, but the frameworks that shape them often originate elsewhere.

That layer does not show up in box scores or recruiting rankings. It shows up earlier, in the assumptions that determine how resources are deployed.

Comments ()